Verification of your sustainability report (CSRD)

The Corporate Sustainability Reporting Directive (CSRD) is an EU regulation that requires companies to regularly publish reports on their environmental, social, and governance (ESG) policies and sustainability efforts. The purpose is to make it transparent for investors, consumers, and decision-makers to assess a company’s sustainability performance, in much the same way as they assess financial performance.

Certified companies already have a clear advantage when it comes to documenting sustainability efforts, supported by a proven system for collecting, managing, and reporting sustainability data.

Companies certified to ISO 9001, ISO 14001, ISO 45001, and ISO 50001 already have the necessary structures, processes, and data in place that can be directly applied to sustainability reporting. This makes it possible to have the sustainability report verified as a natural extension of existing certifications.

We have been approved

by the national accreditation body in Denmark, DANAK. As a result, we are now—similar to auditors and other assurance providers—approved by the Danish Business Authority to carry out verification of companies’ sustainability reports.

In December 2025, Bureau Veritas Denmark received final approval from the national accreditation body in Denmark, DANAK. As a result, we are now—similar to auditors and other assurance providers—approved by the Danish Business Authority to carry out verification of companies’ sustainability reports.

Bureau Veritas Denmark will therefore, as an approved independent assurance provider, be able to issue a verification statement on a company’s sustainability report. Denmark is among the first countries in the EU to grant this type of accreditation, and Bureau Veritas is the first company in Denmark to obtain it.

What do you gain from a verified sustainability report?

- A sustainability account with increased credibility

- More coherent and streamlined internal and external sustainability efforts throughout the year, making data collection, analysis, targets, and action plans more efficient

- A more development-oriented sustainability account that emphasizes progress within the most material sustainability areas

- An independent sustainability assurance statement from an accredited verifier

- Stronger communication with key stakeholders such as customers, employees, and the board through a transparent verification statement that specifically addresses your progress in: stakeholder analysis, double materiality assessment (DMA), the value chain and targets and action plans

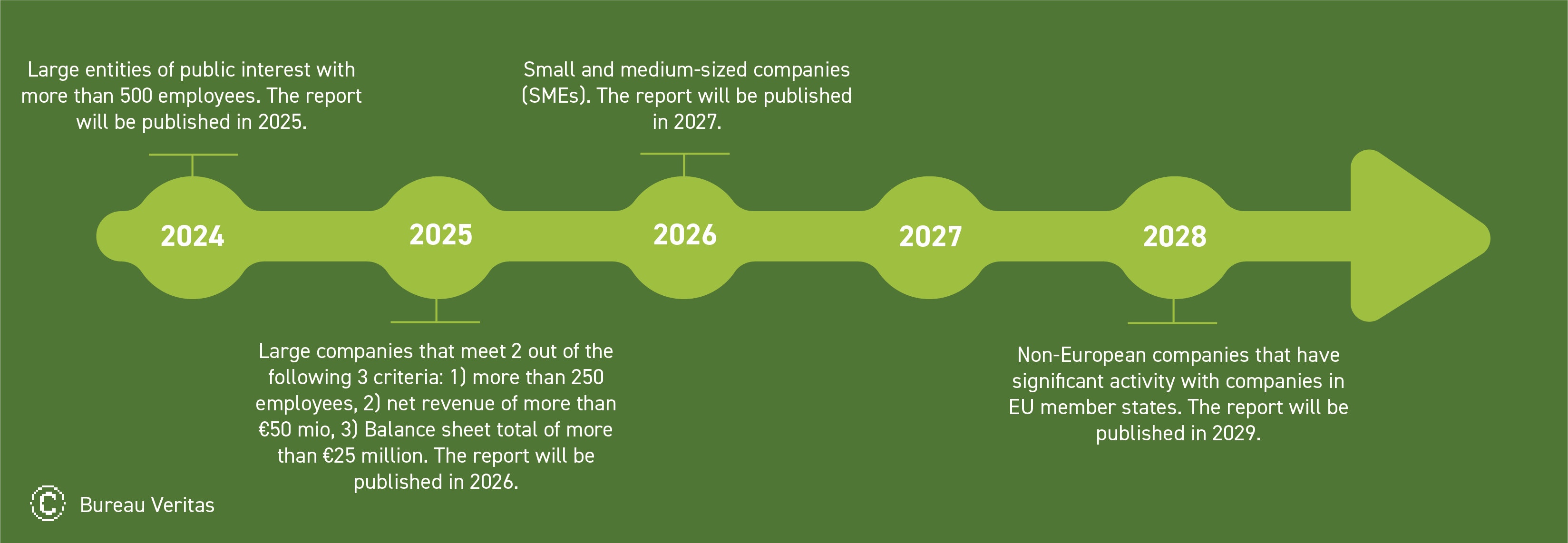

Who does the csrd apply to?

The reporting requirement is updated continuously and will include more and more companies.

The Omnibus Proposal

Please note that the EU Commission’s omnibus proposal from February 2025 introduces a number of changes to the legal requirements listed below. Among other things, sustainability reporting has been put on hold for two years for companies that would otherwise have started reporting under CSRD in 2025 and 2026. In addition, work has begun on revising and simplifying the ESRS standards.

Before the omnibus proposal, the following applied:

Even if a company is not directly covered by the reporting requirement at present, it can be indirectly involved. If partners are covered, they seek information and make demands further through the value chain. The CSRD not only covers the individual company, but also e.g. the company’s chain of sub-suppliers.

On 26 February 2025, the EU issued the Omnibus proposal, which aims to ease and simplify sustainability reporting requirements. The Omnibus proposal is currently in process and is expected to be adopted within 6–9 months. The proposal refers to the voluntary sustainability reporting standard VSME (Voluntary Reporting Standard for SMEs).

how do we report on sustainability?

It is our recommendation that you start by planning how to approach the process. The right prioritisation ensures that you do not go down the wrong track and end up wasting your resources. Bureau Veritas can help you with e.g.:

- Data collection and structuring

- Calculation methods

- How you can involve stakeholders

- And how to ensure a good management system

start with a clarification meeting

Feel free to contact us if you lack knowledge, an overview, and a clarification of where you are now and how best to get started with the very extensive task of reporting. That is what we are here for.

Contact Tomas Jørgensen, Business Developer Sustainability, directly at +45 2684 4199 | tomas.jorgensen@bureauveritas.com or fill out our form.

the 3 first steps

The reporting is very comprehensive and therefore, we have divided the process into 12 steps. The most important first steps are:

- Make sure you get the management's support and commitment in the departments which are key to achieving the reporting goal. The process requires time and collaboration between different employees within e.g. finance, operations, HR, sales, product development and sustainability, and there will be 'bumps' on the road.

- Determine the organisation you wish to report from. This includes both your own organisation, but also your value chain. When it comes to sustainability, it is the company that places the product or service on the market which is responsible for the entire value chain.

- Get an overview of the information you already have. If you base your work on what you already have, you avoid doing the same things twice in the future. Also look at the guidelines within your sector: What is important for that sector?

where can you get help?

At Bureau Veritas, we have a specialist team of sustainability experts (engineers and professionals) working globally. We have a unique understanding and insight that we are happy to make available, both through consultancy, but also through qualifying webinars and courses. Remember to sign up for our newsletter, so you can continually gain knowledge about the area.

We also offer various tools, including:

- GAP analyses which compare company practices and sustainability goals against the known CSRD requirements to clarify any shortcomings.

- Verifications and validations of sustainability data in connection with voluntary declarations, NFRD, which will also apply to the CSRD in the future.

- Training in sustainability.

Our impartiality gives our clients a peace of mind.